Despite record low unemployment, you finally hired one – a diamond in the ruff. After a 16-hour shift on-the-road, his only question at the end of the day was, “What’s next?”

Things are going so smoothly, but then a call from your insurance agent, “The insurance company is hammering me. That new driver you hired has a DUI. They’re asking you to put him in a non-driving capacity or they’re going to reevaluate your insurance program.”

As an insurance agent with many accounts in construction, I’ve had numerous bad-driver scenarios like this. It’s a trend getting hit from two sides with good drivers hard to find in a low unemployment labor pool and increasing auto rates from insurance carriers driving up costs. Thankfully, for commercial insureds, there are solutions to the problem – prevention and alternative insurance options.

Prevent the situation with a Fleet Safety Program. A doctor might tell you prevention is the best medicine and it goes the same with avoiding the hire of a driver with a bad record. Implementing a well thought out Fleet Safety Program will set the standard for your company and, more often than not, keep this problem at bay.

Screening company drivers is the first step to setting up a Fleet Safety Program. “Frequency breeds severity,” is a saying in the insurance industry. If a driver has a history of minor violations or near misses, odds are, at some point, a major incident will occur.

The best tool at the disposal of a business owner to screen employees is a Motor Vehicle Record (MVR). MVR’s are obtained through the Public Abstract Request System (PARS) program with the Wisconsin Department of Transportation. Your company can create an account here and begin screening drivers once they sign a release. There is a cost associated with running records, but nothing overly expensive.

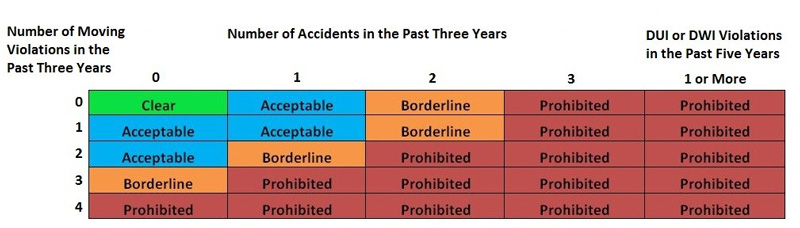

Insurance carriers will want to be sure your drivers fall within a tolerable range of driving violations and accidents. Each company’s standards will be unique to them, but the chart here is an example of a standard the insurance carrier will expect a company to have. It’s recommended you run MVRs on employees once a year, but if you join the PARS program it will notify you if a driver has a violation preventing the need to run MVRs arbitrarily every year.

By Dan Maurer – R&R Insurance

Dan Maurer is a Construction and Manufacturing Specialist with R&R Insurance, an ABC of Wisconsin member company. Learn more about R&R Insurance at www.myknowledgebroker.com.